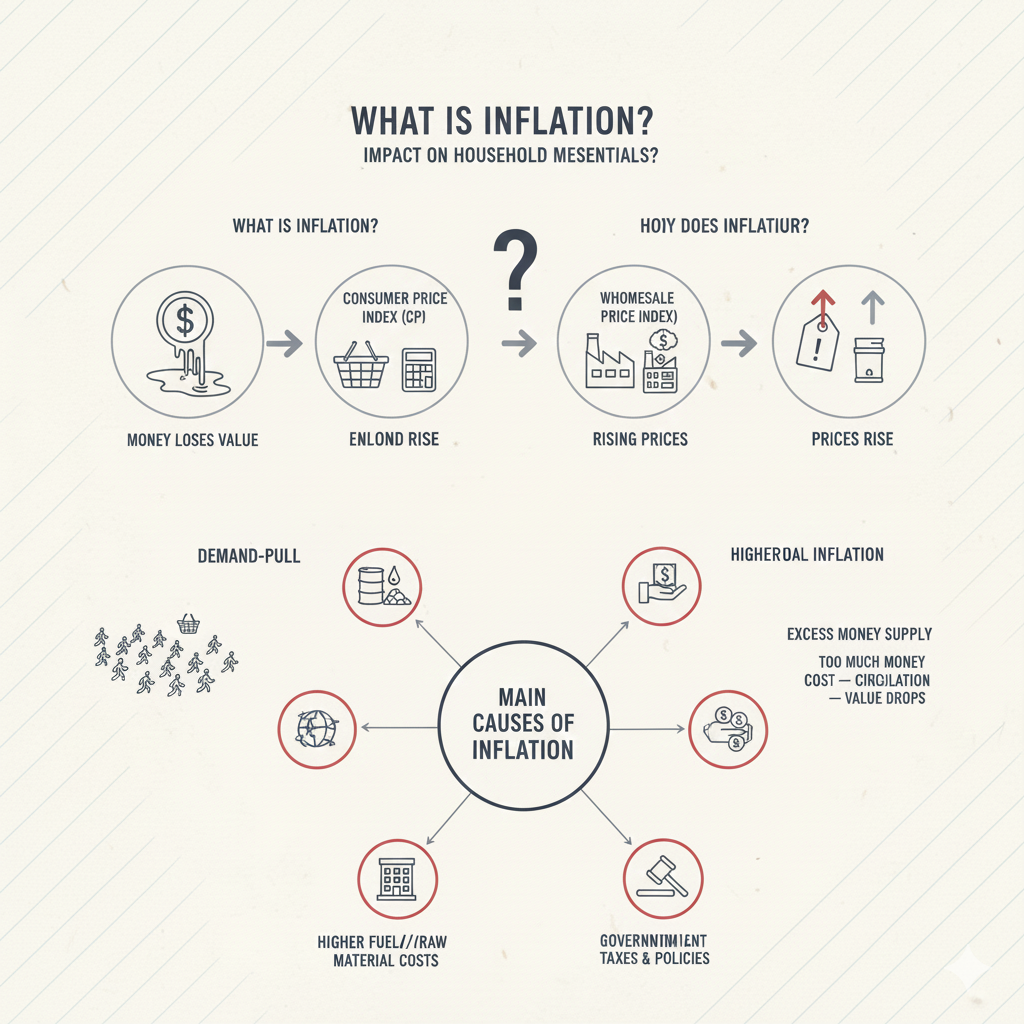

Introduction: Understanding Inflation and the Rising Cost of Living

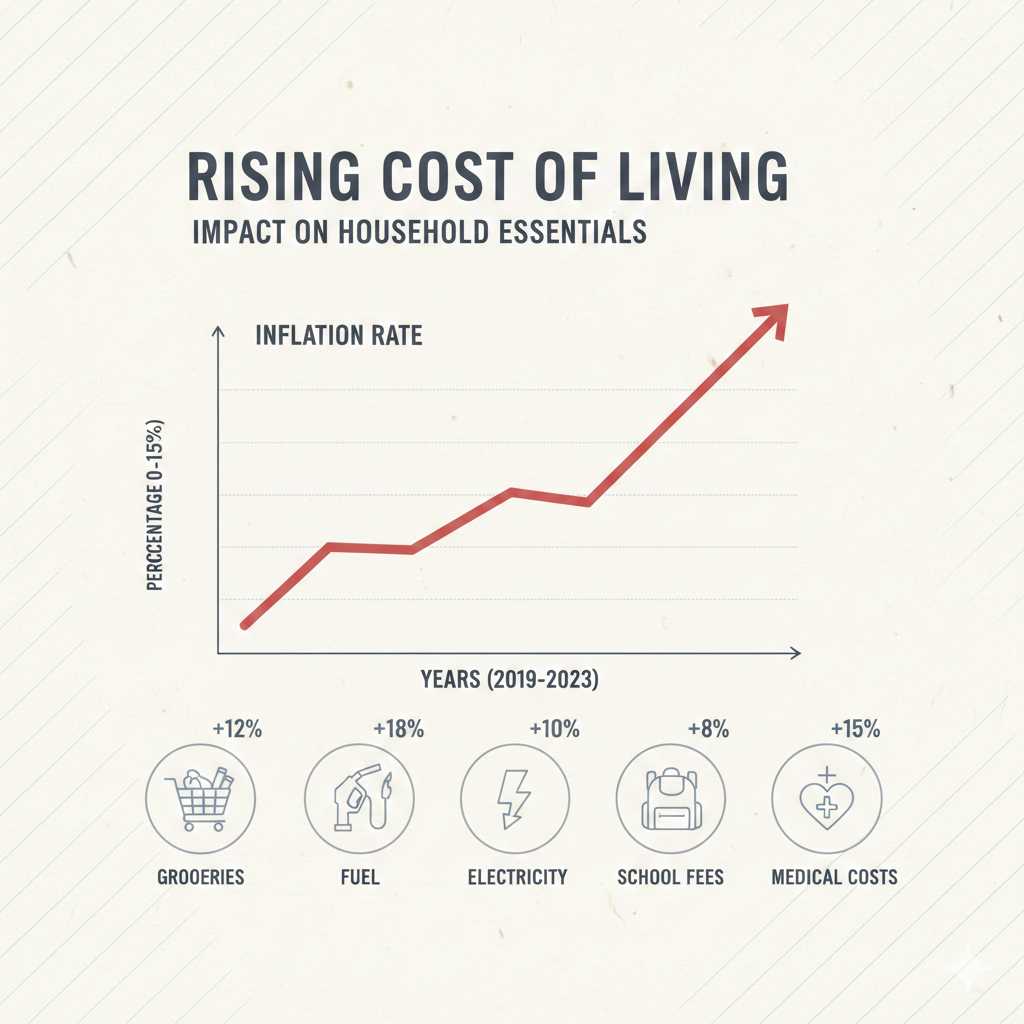

Over the past few years, individuals and families across the world have felt a noticeable shift in their daily expenses. From the price of essential groceries to the cost of transportation, education, healthcare, and household utilities, everything seems to be rising steadily. This continuous increase in prices, commonly known as inflation, has become a central part of everyday conversations. Whether it is around the dinner table, at workplaces, or on social media, people are increasingly concerned about how their income is struggling to keep up with their expenses.

Inflation is not just an economic term used by experts—it is a lived reality for millions of households. When the price of basic goods and services increases, the first impact is felt at home. Budgets begin to tighten, families start adjusting their lifestyle choices, and long-term financial plans often get delayed. Even small adjustments, such as buying less fresh produce, postponing a trip, or cutting down on non-essential items, reflect the silent pressure of the rising cost of living. This pressure is felt even more strongly by fixed-income households, middle-class families, and individuals trying to build savings or invest for the future.

The purpose of this article is not only to explain inflation in simple economic terms but also to connect it with the real challenges faced by everyday people. By understanding how inflation works, why it occurs, and how it spreads through different sectors of the economy, readers can become better prepared to manage their finances. More importantly, this article aims to provide a relatable perspective—highlighting how inflation influences our decisions, our priorities, and even our mindset.

Throughout this article, we will explore the major causes behind inflation, its impact on households, and the changing patterns of spending and saving. We will also look at practical strategies that individuals and families can adopt to cope with rising expenses—ranging from budgeting techniques and spending awareness to long-term planning and alternative income opportunities. Understanding inflation is the first step toward staying financially resilient in a rapidly changing world.

As we begin this journey, remember that inflation is not just an economic phenomenon—it is a personal experience. By becoming aware, adapting wisely, and taking informed decisions, we can protect our financial well-being even in challenging times. Let us now move forward to understand inflation more deeply and explore how we can manage the rising cost of living with clarity and confidence.

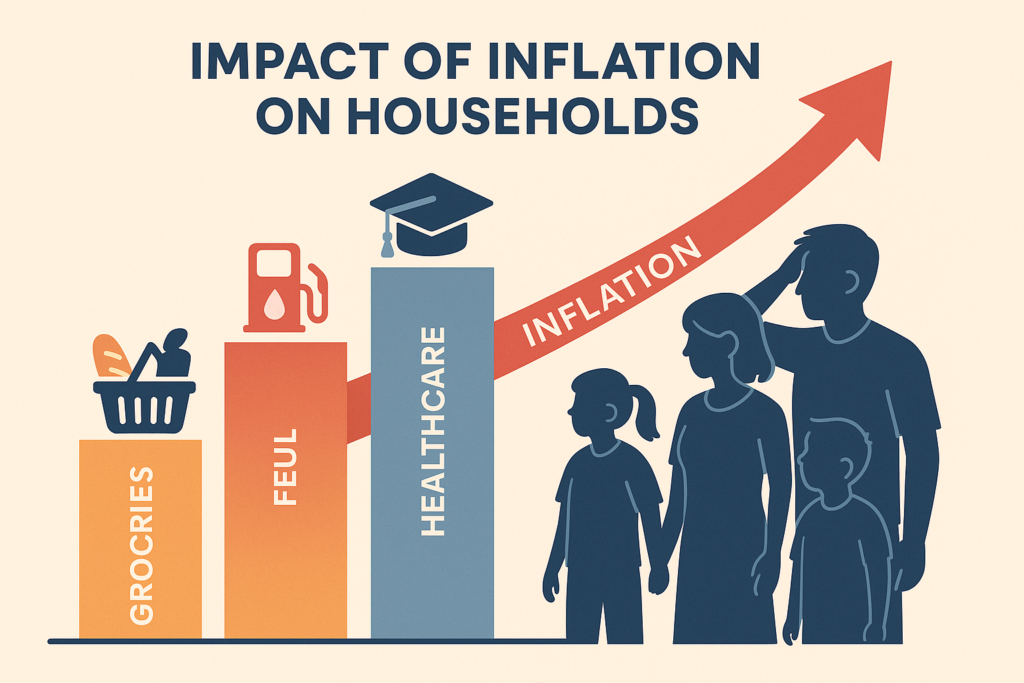

Impact of Inflation on Households

Inflation affects every household differently, but its presence is universally felt. From rising grocery prices to increasing fuel costs and higher expenses on education and healthcare, inflation silently shapes the financial decisions of families. When essential commodities become more expensive, households are forced to rethink their priorities, adjust their lifestyles, and find new ways to manage limited income. Even small changes in the prices of day-to-day items can accumulate steadily, creating noticeable pressure on the monthly budget.

1. Shrinking Monthly Budget

One of the most immediate effects of inflation is the shrinking purchasing power of families. As prices rise, the same income covers fewer expenses than before. A budget that once seemed comfortable suddenly begins to feel restrictive. Households often start cutting back on discretionary spending—such as dining out, entertainment, vacations, or personal purchases—just to make room for essential items like food, fuel, and utility bills.

Many families also experience difficulty in maintaining savings. Funds that were once set aside for emergencies, education, or long-term goals often get diverted toward meeting rising daily expenses. This shift increases financial vulnerability, making households less prepared to handle unexpected events such as medical emergencies or job loss. Over time, this decline in savings can significantly impact future financial security.

2. Changes in Consumer Preferences and Lifestyle

Inflation also influences how people make purchasing decisions. When prices rise sharply, consumers tend to compare brands more frequently, look for discounts, switch to cheaper alternatives, or reduce consumption altogether. A family that previously preferred premium household items may shift to budget-friendly options. Similarly, fresh produce, dairy products, or packaged goods may be bought in smaller quantities to manage costs.

Lifestyle adjustments become unavoidable. For example, families may:

- Limit the use of personal vehicles to reduce fuel expenses.

- Shift to public transportation or carpooling.

- Reduce electricity usage to control utility bills.

- Plan meals more strategically to avoid food waste and overspending.

These changes gradually alter daily routines and habits. Even leisure activities are affected. Outings, movies, subscriptions, and celebrations are often minimized or postponed. Over time, these adjustments can influence the emotional well-being of families as well, especially when cherished traditions or comforts are sacrificed.

3. Rising Pressure on Essential Expenses

Inflation has a deeper impact on essential and unavoidable costs. Education fees, medical bills, house rent, and insurance premiums tend to rise steadily over time. Unlike discretionary expenses, these cannot be easily reduced or avoided. When these costs increase, they disproportionately affect middle-income and lower-income families whose income does not rise as quickly as inflation.

Healthcare is among the most sensitive areas affected by inflation. Even minor increases in consultation fees, medicines, and diagnostic tests can burden the family budget. Similarly, schooling costs such as tuition, books, transportation, and uniforms place additional financial pressure on parents trying to provide quality education for their children.

4. Emotional and Psychological Impact

While inflation is usually described in numbers and percentages, its emotional impact is rarely discussed. Constantly worrying about rising costs can cause stress and anxiety. Families may feel uncertain about their financial future, especially if their income is not increasing at the same pace as prices. This emotional strain affects decision-making and overall mental well-being.

The stress of managing finances with limited resources can also affect relationships within the household. Discussions about money become more frequent, and disagreements about spending priorities may arise. Yet, for many families, such challenges also foster cooperation and unity, encouraging members to support one another and make collective decisions for long-term stability.

Ultimately, inflation reshapes the financial and emotional landscape of households. It challenges families to adapt, prioritize, and plan more carefully. By understanding how inflation impacts different aspects of daily life, households can take proactive steps to protect their financial health and build resilience against future uncertainties.

Practical Solutions: How to Manage Inflation Smartly

Inflation may not be under our direct control, but the way we respond to it can significantly change its impact on our lives. When the cost of living rises, households must adopt smarter strategies, disciplined financial planning, and conscious decision-making. The practical measures below offer a clear roadmap for families trying to stay financially stable despite rising expenses.

1. Reorganize and Review Your Budget

One of the first steps to managing inflation is restructuring the household budget. As prices rise, the old spending pattern becomes unsustainable. A carefully revised budget helps identify wasteful spending and ensures that essential needs are met without financial stress.

How to do it effectively?

- Divide your expenses into three categories: Essential, Important, and Non-Essential.

- Track your monthly expenses and compare them to identify where cuts can be made.

- Reduce discretionary spending like dining out, entertainment, and unused subscriptions.

- Create small monthly targets to manage bigger expenses effectively.

A well-organized budget gives clarity and prevents unnecessary pressure when prices fluctuate.

2. Practice Smart Shopping and Expense Management

Smart shopping is one of the most powerful tools for saving money during inflation. Even minor adjustments in purchasing habits can collectively reduce household expenses by a significant margin.

Smart shopping strategies:

- Buy in bulk: Rice, pulses, detergents, and other essentials cost less when purchased in bulk.

- Use offers and discounts wisely: Buy only the items you genuinely need.

- Choose seasonal and local products: These are fresher and usually cheaper.

- Prepare a shopping list: Helps avoid impulse purchases and stays within budget.

Over time, these small but consistent changes create long-term financial benefits.

3. Build Additional Income Streams

When inflation rises faster than income, the most effective solution is to explore alternative sources of earning. Even a small additional income stream can greatly reduce financial pressure and improve household stability.

Possible income opportunities:

- Freelancing work such as writing, design, marketing, or video editing.

- Small home-based businesses — baking, tiffin services, homemade products, tutoring.

- Skill-based services — graphic design, digital marketing, consulting.

- Renting out items such as tools, cameras, or small equipment.

Diversifying income strengthens financial resilience and creates a safety net during difficult times.

4. Long-Term Saving and Investment Strategies

Inflation reduces the real value of money, which means traditional savings alone are not sufficient. To secure the future, families must adopt investment strategies that offer returns higher than the inflation rate.

Recommended options:

- SIP in mutual funds: A reliable way to beat inflation in the long run.

- PPF/EPF and other government-backed schemes: Safe options with tax benefits.

- Health insurance: Protects against unpredictable medical expenses.

- Emergency fund: Keep savings equal to at least 6 months of essential expenses.

A balanced investment portfolio provides financial security and cushions against rising costs.

5. Reduce Consumption of Energy and Resources

Managing electricity, water, and fuel consumption can bring noticeable savings. These are recurring expenses, and optimizing them can significantly lower the monthly financial burden.

Practical tips:

- Use LED bulbs and energy-efficient appliances.

- Turn off unnecessary lights and fans when not in use.

- Practice water-saving methods inside the home.

- Adopt carpooling or switch to public transport when possible.

Small mindful habits contribute to long-term financial improvement.

6. Manage Debt Wisely

Debt can become more challenging to handle during inflation, especially if interest rates rise. Without proper management, it can lead to severe financial stress. Therefore, evaluating and optimizing debt obligations becomes essential.

Effective debt management tips:

- Prioritize high-interest loans and repay them first.

- Limit credit card usage to avoid accumulating costly debt.

- Consider refinancing options if interest rates are high.

- Ensure EMIs do not exceed 30–40% of your monthly income.

A disciplined approach to managing loans protects families from financial instability.

7. Increase Self-Reliance

During inflation, becoming more self-reliant can significantly reduce day-to-day expenses. Simple lifestyle changes can help families avoid unnecessary spending.

Self-reliance ideas:

- Grow small vegetables or herbs at home.

- Cook meals at home instead of frequently eating outside.

- Learn basic repair skills to avoid costly services.

- Reuse and recycle household items creatively.

Ultimately, inflation teaches us to be resourceful, mindful, and financially disciplined. With the right strategies, families can not only survive inflation but also become stronger and more resilient.